#004 | The 3 Fund Portfolio

How to build a winning investment portfolio with only 3 holdings

Hey friends,

Are you looking for ways to build an investment portfolio that’s low-maintenance, doesn’t compromise your returns, and has stood the test of time?

If so, you’ve come to the right place!

Today’s article will be breaking down everything you need to know about the three-fund portfolio, which is one of the easiest ways to start building up your personal asset column.

Its key benefits include:

Simplicity: It eliminates the need for constant portfolio monitoring and rebalancing. You can also “set it and forget it” by pairing it with an automated dollar-cost averaging program.

Diversification: By spreading your investments across different asset classes and countries, you reduce the risk exposure you have to any single holding.

Cost Efficiency: Index funds typically have lower fees than actively managed funds, which allows you to keep more money in your pocket.

Long-term emphasis: This approach encourages a disciplined, long-term perspective. Investors are less incentivized to make impulsive trades based on short-term market fluctuations.

Unfortunately, many people fall victim to the allure of active investing and beating the market.

Investors frequently attempt to pick the stocks and fund managers who will outperform, but they rarely succeed on a consistent basis. There are two primary reasons for this.

Actively managed funds charge ~5x more in fees for a 13% chance of beating the market

Active managers of large-cap domestic equity funds outperformed the S&P 500 in only 3 of the last 23 years.

This means that 87% of the time, active managers of these funds underperformed the index.

Not only did actively managed funds produce lower returns - they also charged more fees than index funds.

In 2022, active funds averaged an asset-weighted fee of 0.59%, while passive funds averaged a 0.12% fee.

“The more complicated your portfolio is, the more expensive and more prone to blow-ups it's likely to be -- which also increases the odds that it will generate subpar returns.”

- Walter Updegrave, “The only funds you need in your portfolio now”, CNN Money

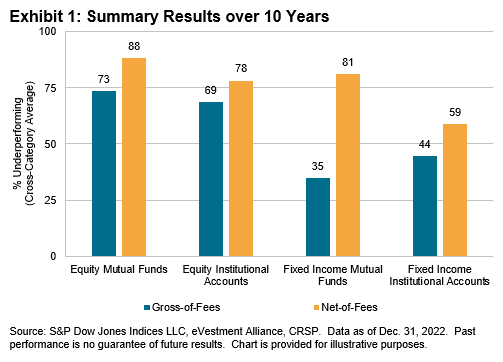

The visualization below further displays how active funds underperformed before and after fees. As you can see, most active stock and bond funds had no edge over their benchmarks.

Luckily, investors can increase their probability of success by adopting the three-fund portfolio, a passive investing strategy that aims to match the performance of an index.

Building your three-fund portfolio

The three holdings needed for this portfolio are a U.S. total stock market index fund, a U.S. total bond market index fund, and an international total stock market index fund.

For simplicity, I will provide examples of a Vanguard ETF and mutual fund for each holding. It’s important to note, however, that there are plenty of other funds available that achieve a similar outcome.

Fund 1: U.S. Stock Index (Tickers VTI or VTSAX)

This provides exposure to the entire U.S. stock market, capturing the performance of both large and small-cap stocks.

Generally, stocks will have higher risk and return profiles than bonds over the long term.

Fund 2: U.S. Bond Index (Tickers BND or VBTLX)

For stability and income in your portfolio, this fund provides exposure to a mix of government, corporate, and other bonds.

Fund 3: International Stock Index (Tickers VXUS or VTIAX)

This fund adds global diversification by investing in international stocks.

At the time of writing this, the geographies covered by VXUS include Europe, Asia-Pacific, Emerging Markets, North America, and the Middle East.

“Don’t look for the needle in the haystack. Just buy the haystack!”

- John C. Bogle, Founder of The Vanguard Group

Your asset allocation determines the weight of each fund in your portfolio

There are two general rules of thumb for asset allocation:

“Age in bonds” rule: your age equals the percent of bonds to hold

Stocks: 100% less your current age

If you are 30 years old, this implies an asset allocation of 30% bonds and 70% U.S. and international stocks.

Keep in mind this is only a rule of thumb though - if you’re 30, you may actually prefer 60% stocks and 40% bonds, or even 90% stocks and 10% bonds.

Your optimal asset allocation is not solely based on your age. There are many other factors to consider, some of which include your goals, risk tolerance, time horizon, and income needs.

The tradeoffs of the three-fund portfolio

If you are determined to roll the dice and try beating the market, this will not be the right approach for you. The nature of the three-fund portfolio is to match the market, not outperform it.

Additionally, it misses out on other asset classes that may add another layer of diversification to your portfolio. The three-fund portfolio doesn’t have exposure to real estate, REITs, commodities, cryptos, derivatives, or any other asset class. It is strictly limited to stocks and U.S. bonds.

Finally, you are responsible for rebalancing your portfolio. By investing in target date funds, a fund manager can rebalance your portfolio for you.

Conclusion

The three-fund portfolio is a time-tested concept that allows you to build a low-cost and well-diversified investment portfolio.

Despite its simplicity, data shows that this approach has historically outperformed actively managed funds.

My favorite part of the three-fund portfolio is that it’s great for lazy people like myself.

It can be easily automated with a dollar-cost averaging program, which can make it totally hands-off and put your wealth-building on autopilot.

That’s all for today - thank you for taking the time to read!

Subscribe to "The Asset Column" to have future publications delivered straight to your email inbox.

Follow us on Twitter/X, where we post daily content about personal finance, investing, and entrepreneurship.

Share the asset column with friends and family if you learned something!

Refer to the disclaimer on our “About” page.